GET YOUR FREE PDF REPORT!

The Definitive

Kansas City

Home Buying Guide

A comprehensive, market-specific reference for every type of buyer — from first-timers navigating their first offer to investors underwriting their fifth rental. Written by the team at Reco Real Estate Advisors with one goal: give you real knowledge, not generic checklists.

What's Inside

Use the sections below to jump to what matters most. First-timers: read cover to cover. Investors: start with Section 3 and Chapter D. Relocators: begin with Section 2 and the county profiles.

Built on Market Intelligence. Driven by Results.

At Reco Real Estate Advisors, we don't believe in generic real estate advice. We believe in knowing the Kansas City market deeper than anyone else in it — the neighborhoods, the economics, the schools, the investment fundamentals — and putting that knowledge to work for every client we represent.

Whether you're purchasing your first home in Olathe, acquiring a hospitality asset across the metro, or building a residential portfolio in Jackson County, our team brings the same analytical discipline and market depth to every transaction.

Kansas City is one of the most undervalued real estate markets in the country. We consider it our job to make sure our clients capture that advantage — every time.

Achievements & Recognitions

KW Overland Park · KC Metro

What We Do

Full-service real estate advisory across every asset class and transaction type in the Kansas City metro.

The Reco Team

Five specialists. One integrated team. Every discipline covered in-house.

Talk to our team — no obligation, just a real conversation about your goals.

Welcome & How to Use This Guide

At Reco Real Estate Advisors, we believe the best transactions happen when buyers arrive educated. Not just about the process — about the market. Too many buyers walk into one of the most consequential financial decisions of their lives with information scraped from Zillow and a half-remembered conversation with a coworker who bought a house three years ago. We built this guide to change that.

This is not a checklist. It's not a legal disclaimer dressed up as advice. It's what we'd tell you if you sat across from us in our office on day one — the real picture of the Kansas City metro, the transaction process as it actually works here, and the honest pros and cons of every major market you might be considering. We've written it to serve multiple types of buyers simultaneously, because the KC metro attracts all of them.

How to Navigate This Guide

- First-time buyers: Read it cover to cover. The process section (Section 4) and your buyer-type chapter (Chapter A in Section 5) are foundational. Don't skip the glossary in Section 7 — know the terms before you need them.

- Upsizers and downsizers: You know the process; what you need is the market. Dive into Section 3 for the county-by-county data, then your buyer chapter in Section 5.

- Rental property investors: Start with the Big Picture in Section 2 (Kansas vs. Missouri dynamics matter), then go straight to Section 3's investor data fields for each area, and Chapter D in Section 5.

- Relocation buyers: Begin with Section 2 — the KC geography orientation — then read the county overviews in Section 3 to shortlist where you want to land. Chapter E in Section 5 is written for you.

- Luxury buyers: The Johnson County deep-dive in Section 3 and Chapter F in Section 5 are your primary resources.

The Dual-State Reality

The Kansas City metro straddles two states — and that's not just geography, it's finance, law, and lifestyle. Kansas and Missouri operate under different property tax structures, different income tax regimes, different landlord-tenant laws, different school funding models, and different MLS conventions.

When you ask "where should I buy in KC?" the answer isn't just a neighborhood — it's a state. We'll give you the full picture throughout this guide so you can make that call with open eyes.

About Reco Real Estate Advisors

Reco Real Estate Advisors is a KW Partners affiliate serving the Kansas City metro. We operate at the intersection of commercial intelligence and residential service — meaning our team brings investment analysis, market data fluency, and negotiation discipline to every transaction, whether it's a first home or a five-property portfolio.

Reco serves buyers across the full Kansas City metro — both Kansas and Missouri sides — with deep expertise in Johnson County KS luxury residential, KC metro commercial, investment properties, multifamily assets, and Midwest hospitality real estate. Every client benefits from the same institutional analytical lens regardless of transaction size.

Understanding the KC Metro — Big Picture

Before you look at a single listing, you need to understand what kind of market you're entering. Kansas City is not one market — it's seven counties, two states, dozens of school districts, and hundreds of zip codes, all behaving differently at any given moment.

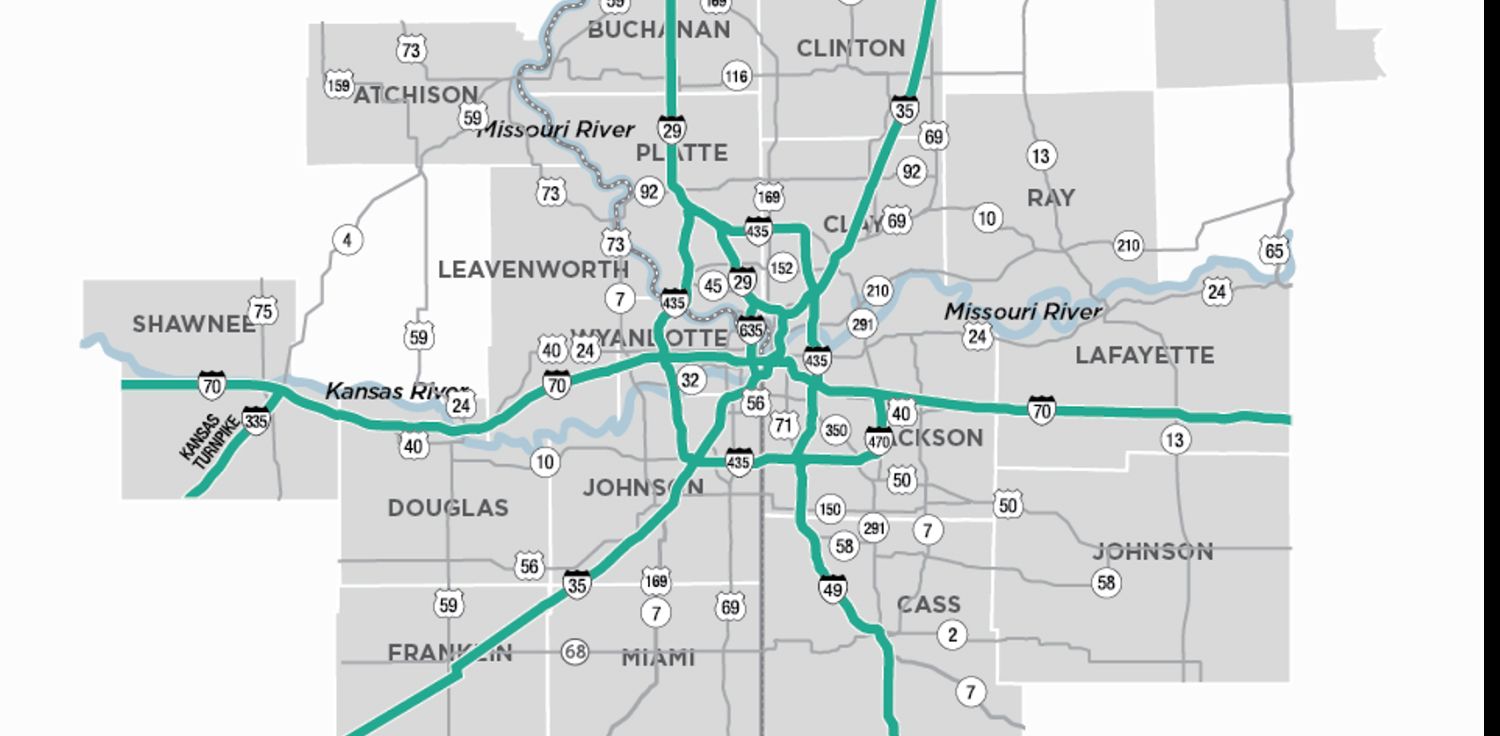

The KC Metro Geography

The Kansas City metro spans approximately 7,000 square miles across Missouri and Kansas with a combined population nearing 2.2 million. The Missouri River bisects the metro east-to-west; the state line runs north-to-south through the center of the urban core.

Four interstates define how the metro moves and where people live relative to where they work:

- I-35 — the north-south spine of the Kansas side, connecting Olathe, Overland Park, and Lenexa southward to Gardner and beyond, and north toward downtown KC and eventually the Northland.

- I-70 — the primary east-west corridor. It splits downtown KC, carries traffic through Independence and Blue Springs on the Missouri side, and crosses into KCK on the Kansas side.

- I-435 — the circumferential beltway looping around the southern and eastern metro. It's the commuter ring that makes south Johnson County and south KC metro accessible without touching downtown.

- I-470 — the southern Missouri bypass, connecting Lee's Summit, Raytown, and the Independence corridor. Critical for Cass County buyers commuting north.

Understanding these routes isn't just trivia. Where you live relative to your employer along these corridors is the single biggest quality-of-life variable for most KC buyers.

Kansas vs. Missouri Side

This distinction shapes everything from your monthly payment to your estate plan.

Property Taxes: Johnson County KS typically runs 1.2%–1.5% effective rate on assessed value. Jackson County MO runs 1.0%–1.4%, though assessment practices vary widely. Wyandotte County KS can be higher relative to home values. Always run the actual annual tax estimate on any home you're considering — it can swing your monthly payment by $300–$500+.

Income Taxes: Kansas has a flat-ish income tax structure with rates topping around 5.7%. Missouri tops out near 4.95%. For high-income earners, this difference is real money annually. Consult your CPA — some buyers specifically choose one side of the state line for tax optimization.

School Funding: Kansas funds schools heavily through property taxes, which is why Blue Valley USD and Shawnee Mission USD in Johnson County are so well-resourced — the tax base supports it. Missouri districts are more variable, with state funding formulas that create wider gaps between districts.

HOA Culture: Far more prevalent on the Kansas side, particularly in Johnson County. You will almost certainly buy into an HOA if you're purchasing a new-construction or post-1990 home in Overland Park, Olathe, or Lenexa. Missouri side HOAs exist but are less universal.

Landlord Law: Missouri is more landlord-friendly than Kansas, with shorter statutory eviction timelines — a real consideration for investors choosing a state to build a portfolio.

Current Market Conditions

The KC metro has experienced sustained appreciation since 2019, with inventory remaining tight across most submarkets. Buyers should confirm current MLS data with their agent — the figures below are directional benchmarks reflecting 2024–2025 trends. Always ask your agent for live days-on-market and months-of-supply data before making a pricing decision.

2026 Price Performance by Submarket

Source: KCRAR, Redfin, NAR · Q1 2026 · Confirm current data with your agent.

| Submarket | Median Price | YoY Change | Avg. DOM |

|---|---|---|---|

| Leawood, KS | $650,000+ | +3.8% | 28 |

| Overland Park, KS | $485,000 | +4.1% | 34 |

| Prairie Village, KS | $410,000 | +4.0% | 32 |

| Olathe, KS | $375,000 | +5.2% | 38 |

| Lenexa / Shawnee, KS | $360,000 | +4.8% | 40 |

| Lee's Summit, MO | $320,000 | +5.0% | 42 |

| Blue Springs, MO | $270,000 | +4.5% | 46 |

| N. Kansas City, MO | $210,000 | +7.1% | 51 |

Why Relocators Choose Kansas City

KC consistently ranks among the top 10 most affordable major metros in the country — but "affordable" undersells it. You're not trading down in lifestyle; you're getting more of it for less money.

- Cost of living: Housing costs run roughly 30–40% below the national average for comparable home sizes. A $450,000 home in Johnson County would be $800,000–$1.2M in Denver, Austin, or Nashville for equivalent quality and schools.

- Job market: Anchored by healthcare (HCA Midwest, KU Health System, Children's Mercy), tech (Cerner/Oracle Health, Garmin, T-Mobile HQ in Overland Park), financial services (UMB, Commerce Bank, Nuveen/TIAA), and logistics (KC sits at the geographic center of the US — FedEx, UPS, and freight networks love it).

- Airport access: KCI (Kansas City International) completed a brand-new single terminal in 2023. Nonstop routes to 60+ destinations. For business travelers, it's a genuine competitive advantage over markets where the airport is 45 minutes away and miserable.

- Sports culture: The Chiefs (back-to-back-to-back Super Bowl contenders), the Royals (storied franchise), and the KC Current (NWSL powerhouse with a purpose-built stadium) give KC a sports identity that punches above its population weight.

- Food & arts: KC barbecue is world-class and not a cliché. The restaurant scene — from the 18th & Vine jazz corridor to the Crossroads Arts District to Westport — is legitimate. The Nelson-Atkins Museum of Art and the Kauffman Center for the Performing Arts are nationally recognized institutions.

KC Seasonal Market Patterns

The KC real estate market is highly seasonal. Knowing the calendar gives you a strategic edge.

Market Intelligence by County and Area

This is the intelligence you'll come back to repeatedly. Every county and area profile follows the same format so you can compare apples to apples. Data is directional — confirm current figures with your Reco agent before making any pricing or investment decision.

Johnson County, Kansas

The flagship county of the KC metro — highest median incomes, top-ranked schools, dominant luxury market, and the economic engine of the Kansas side.

Johnson County is the wealthiest county in Kansas and one of the wealthiest in the Midwest. It's anchored by two powerhouse school districts — Blue Valley USD 229 and Shawnee Mission USD 512 — that consistently rank among the top in the state and draw families from across the metro and from out of state. The county's corporate base along the I-435/Metcalf corridor (T-Mobile HQ, Garmin, Black & Veatch, Cerner/Oracle Health) means short commutes for thousands of white-collar professionals who also want elite schools and well-maintained neighborhoods.

HOAs are the norm here. Covenant restrictions keep neighborhoods cohesive but also limit what you can do with your property. Buyers from other parts of the country often find Johnson County's HOA culture more intense than they expected — read the CC&Rs before you close, not after.

The county's growth corridor has been pushing south and southwest — Gardner and Spring Hill are the current frontier of affordability within JoCo. The northern tier (Prairie Village, Mission, Merriam) offers older, often more characterful housing stock at prices that look attractive relative to Overland Park's new-construction product.

Overland Park

Overland Park is the second-largest city in Kansas and the commercial heart of Johnson County. It's not one neighborhood — it's a sprawling city that spans dramatically different product types and price points depending on where you are within it. Treat it as three distinct sub-markets: North OP, Central OP, and South OP.

North Overland Park (roughly north of 95th St)

Character: Older, more established neighborhoods with mature trees and stronger community identity. Proximity to Prairie Village and the Country Club Plaza gives North OP a character distinct from the new-construction suburban feel of the south. Ranch homes, split-levels, and mid-century two-stories from the 1960s–1980s are the dominant stock.

Housing Stock: 1,200–2,200 sq ft ranches and two-stories, built primarily 1965–1995. Expect deferred maintenance items on older mechanicals — sewer scopes and radon tests are essential here. Some infill patio homes and newer townhomes near major retail corridors.

Price Range: Starter: $250K–$325K. Mid: $325K–$475K. Renovation plays can start in the $220s.

Days on Market: Fast — typically 10–21 days for well-priced homes. Well below metro average.

Appreciation: Moderate-to-strong. The proximity to Prairie Village and the character of the older housing stock has driven consistent demand.

School Information

North OP straddles the Shawnee Mission USD 512 boundary. Elementary schools within SM include Shawnee Mission East and Shawnee Mission North feeder schools — ask your agent for the exact attendance boundary for any home you're considering, as these have shifted. Niche rates many SMSD elementaries highly. Private options: Cure of Ars School, Pembroke Hill (nearby), Notre Dame de Sion.

Lifestyle & Amenities

Excellent restaurant access via 119th Street and Metcalf Avenue corridors. Nearby Corbin Park and Town Center Plaza for retail. Johnson County Park system provides trails and parks throughout. Commute to downtown KC: 20–30 minutes via I-35 or Metcalf. KU Med corridor: 15–25 minutes.

✓ Pros

- Mature trees, established neighborhood character

- More affordable entry points than south OP

- SMSD school system access

- Strong appreciation history on renovated homes

- Good commute access via I-35 and Metcalf

- Less HOA intensity than south OP subdivisions

✗ Cons

- Aging infrastructure — sewer laterals often need attention

- Radon levels elevated — test every home

- Less new construction; renovation required to modernize

- Some areas feel dated relative to price point

- Traffic on Metcalf can be brutal during peak hours

Buyer-Type Fit

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Strong | Good inventory under $300K; lower property taxes vs. Missouri side for same quality |

| Upsizer | Moderate | Move-up inventory exists but competition is fierce; better upsize value in central OP |

| Downsizer | Moderate | Some patio home options; not as many condo/townhome choices as south OP |

| Investor | Strong | BRRRR plays on older ranches; renovation adds meaningful value; rental demand solid |

| Luxury | Low | Price ceiling here; luxury buyers should look central/south OP or Leawood |

| Relocator | Strong | Accessible price point for KC newcomers; SMSD schools a major draw |

💼 Investor Data — North Overland Park

STR Viability: Limited — Overland Park has STR registration requirements and most HOAs restrict short-term rentals. Long-term rental is the play. BRRRR Opportunity: Strong on distressed 1960s–1980s ranches that can be renovated and refinanced. Watch sewer lateral replacement costs ($5K–$15K) in your renovation budget. City Registration: Overland Park requires rental property registration and periodic inspections.

Central Overland Park (95th St to 135th St)

Character: The corporate core of JoCo. Home to T-Mobile's campus, major retail at Corporate Woods and Corbin Park, and a mix of planned subdivisions from the 1980s–2000s. This area is exceptionally convenient but can feel more suburban-corporate than the north or south ends of OP.

Housing Stock: 1,500–2,800 sq ft two-stories and ranches, 1985–2005 construction. Many subdivisions with active HOAs. Some newer townhome communities near retail corridors.

Price Range: Mid: $350K–$500K. Move-up: $500K–$700K. Entry: $280K–$350K.

Days on Market: Fast — 12–24 days for well-priced product.

Schools: Primarily Blue Valley USD 229 in the southern half, Shawnee Mission in the northern half. Ask for the exact feeder school for any address. Blue Valley schools are nationally ranked — this is a major driver of demand in this price tier.

Lifestyle: Extremely car-dependent. Best-in-class suburban retail and dining. Commute to downtown KC 25–35 minutes. T-Mobile campus and Cerner/Oracle Health within 10–15 minutes of most addresses.

✓ Pros

- Blue Valley USD access — top-ranked schools

- Short commute to JoCo corporate corridor

- Excellent retail and dining within 5 minutes

- Well-maintained planned neighborhoods

- Strong long-term appreciation

✗ Cons

- Heavily car-dependent; minimal walkability

- HOA restrictions can be strict and costly

- Suburban sameness — neighborhoods feel similar

- Traffic on Metcalf/119th/135th intersections

💼 Investor Data — Central Overland Park

Blue Valley schools drive strong rental demand from families who can't yet afford to buy in the district. Cap rates compressed vs. north OP due to higher purchase prices. Long-term appreciation story is stronger than cash flow story here. HOA fees typically $50–$150/month — factor into your analysis.

South Overland Park (south of 135th St)

Character: The newest growth frontier of the KC suburban landscape. South OP — including areas like Wolf Run, Lionsgate, Nottingham Forest, and new communities extending toward 179th Street — is where you find the most recent construction, the biggest lots in the outer rings, and the highest concentration of luxury new-build product in the metro.

Housing Stock: Predominantly post-2005 construction. New-build communities from builders like Rodrock Homes, James Engle Custom Homes, and Starr Homes. Lot sizes range from 1/4 acre in denser subdivisions to 1+ acre estate lots near 167th–179th Street.

Price Range: Entry new construction: $475K–$600K. Mid-tier move-up: $600K–$900K. Luxury estates: $900K–$2M+.

Days on Market: Moderate — 20–35 days. Higher price points mean longer marketing windows.

Schools: Almost entirely Blue Valley USD 229. Blue Valley North, Blue Valley Southwest, and Blue Valley West high schools serve this area. BV is routinely ranked among Kansas's top 5 districts statewide.

Lifestyle: This is the lifestyle many KC families are aspirationally working toward. Beautiful, planned communities with pools, walking trails, and community amenities. Car-dependent by design. New retail follows growth here — the 159th Street corridor has become a secondary commercial spine. Commute to downtown KC is 35–45 minutes — the tradeoff for this lifestyle is distance.

✓ Pros

- Best new construction product in the metro at this price point

- Blue Valley USD — one of Kansas's best districts

- Larger lots and newer mechanicals vs. north OP

- Community amenities (pools, trails, ponds) built in

- Strong resale market driven by continued growth

- Low crime rates; high community investment

✗ Cons

- Longest commute in Johnson County to downtown KC

- New construction quality varies by builder — vet thoroughly

- HOA fees can be $150–$400/month in amenity-heavy communities

- Limited character — many neighborhoods look similar

- Some flood risk in lower elevation areas near creeks

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Low | Price points start too high for most first-timers |

| Upsizer | Strong | The primary destination for JoCo move-up buyers with children |

| Downsizer | Moderate | Maintenance-free patio home communities exist; lot of stairs in 2-story product |

| Investor | Low | Cap rates very compressed; not a cash flow play |

| Luxury | Strong | Best luxury new construction in the KC metro |

| Relocator | Strong | Families relocating for school district quality come here |

💼 Investor Data — South Overland Park

Cap rates are the lowest in the metro here. This is an appreciation play, not a cash flow play. Corporate relocation executives seeking temporary housing drive the luxury rental demand. STR largely prohibited by HOA covenants. Unless you're banking on significant appreciation, other submarkets offer better investment returns.

Leawood

Character: Leawood is the most prestigious residential address in the KC metro — a well-planned, mature community with exceptional infrastructure, high household incomes, and a deep bench of luxury housing stock. The Ranch Club, Iron Horse, Hallbrook Farms, and Mission Hills Drive neighborhoods are where KC's medical, legal, and business elite live. Leawood is not flashy about its affluence — it's understated, private, and self-sustaining.

Housing Stock: The breadth here is wider than most buyers expect. The eastern edge near State Line Road offers 1970s–1990s ranch and two-story product in the $450K–$650K range. The western and southern tiers — Iron Horse, Ranch Club, Hallbrook — are $800K–$4M+ estates on large, heavily landscaped lots.

Price Range: Entry: $400K–$600K. Mid luxury: $700K–$1.2M. Upper luxury: $1.2M–$4M+.

Days on Market: Moderate — luxury product typically 30–60 days. Entry-level Leawood moves faster.

Appreciation: Strong and consistent. Leawood has proven resilient through market cycles due to the depth and quality of its buyer pool.

School Information

Shawnee Mission USD 512 serves most of Leawood, with Leawood Elementary and Leawood Middle School having strong reputations. Shawnee Mission East High School feeds from here and is among the most academically regarded public high schools on the Kansas side. Private options within 10 minutes: Pembroke Hill, Notre Dame de Sion, Saint Thomas Aquinas (Olathe).

Lifestyle & Amenities

Town Center Crossing and Leawood Town Center deliver the metro's highest concentration of luxury retail, dining, and services — Nordstrom, Macy's, The Capital Grille, and dozens of independents. Hallbrook Country Club and Leawood South Country Club provide private golf access. The KC Art Institute and Nelson-Atkins are 20 minutes north. Commute to downtown KC: 25–35 minutes. KU Health System: 20–25 minutes.

✓ Pros

- Prestige address with strong resale value floor

- Best luxury housing stock in the metro

- Excellent schools (SMSD) and private school proximity

- Best retail and dining corridor in JoCo

- Quiet, private, masterplanned luxury neighborhoods

- Low crime; high community investment

✗ Cons

- Entry price is high — limited product below $400K

- HOA fees in luxury communities run $300–$800+/month

- Very car-dependent; minimal walkability

- Less diversity than other KC submarkets

- Dated interiors common in 1990s luxury stock

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Low | Not the market — price points start high |

| Upsizer | Strong | The aspirational move-up destination for JoCo buyers |

| Downsizer | Strong | Excellent maintenance-free condo and patio home options near Town Center |

| Investor | Low | Cap rates barely pencil; not an investor's market |

| Luxury | Strong | Top luxury market in KC metro — deep, quality inventory |

| Relocator | Strong | The "safe choice" for corporate relos who want the best address without research risk |

💼 Investor Data — Leawood

Leawood is an appreciation play, full stop. Cap rates are among the lowest in the metro. The investment thesis is capital preservation and long-term appreciation in a high-barrier-to-entry submarket. Corporate relocation temporary housing is the primary rental play at the luxury tier. HOAs and high property taxes make the math difficult for traditional rental investors.

Prairie Village

Character: Prairie Village is the most walkable, most neighborhood-centric community in Johnson County — and increasingly, in the entire metro. Built primarily in the 1950s and 1960s as KC's first wave of suburban development, PV has the bones of a traditional town: the Prairie Village Shopping Center with its independent restaurants and shops, tree-lined streets, and a genuinely strong sense of community identity. It's attracted a wave of renovation-minded buyers over the past decade who see the value in its location, character, and school access.

Housing Stock: Predominantly 1,000–2,000 sq ft ranch homes and Cape Cods from the 1950s–1970s. Many have been renovated to high standards — open kitchens, updated baths, modern finishes in older footprints. Buyers should understand they're paying for location and schools, not square footage.

Price Range: Entry: $350K–$450K. Mid: $450K–$650K. Fully renovated premium: $650K–$900K.

Days on Market: Very fast — Prairie Village routinely leads Johnson County in quick sales. Well-renovated homes can see 5–10 offers within the first weekend.

Appreciation: Strong. PV's desirability has only increased as the urban-lifestyle demographic has grown.

School Information

Shawnee Mission USD 512 exclusively. Corinth Elementary and Brookwood Elementary are highly regarded. Shawnee Mission East High School — perhaps the most academically prestigious public high school on the Kansas side — serves the eastern PV neighborhoods. SM East's IB programme and strong arts programs are a significant draw.

Lifestyle & Amenities

The Prairie Village Shopping Center — Hen House Market, multiple independent restaurants, and service businesses — is a genuine walkable retail node. The 91st and Mission Road corridor offers additional dining. Corinth Hills neighborhood has access to Johnson County's trail system. Proximity to Leawood's Town Center for higher-end retail. Commute to downtown KC: 20–28 minutes via I-35 or Ward Parkway.

✓ Pros

- Best walkability in Johnson County

- Strong neighborhood identity and community events

- SM East feeder schools — top-tier academics

- Renovation potential in original stock

- Proximity to both KCMO character neighborhoods and JoCo amenities

- Strong resale demand — rarely a slow market

✗ Cons

- Small square footage relative to price — sticker shock for buyers from other markets

- Competition is fierce; be prepared for multiple offers

- Older mechanical systems — full inspection essential

- Limited parking in renovated areas near shopping

- Radon testing strongly advised — elevated risk in older homes

💼 Investor Data — Prairie Village

Excellent rental demand driven by SM East school district seekers who aren't ready to buy. BRRRR potential on unrenovated ranches — the renovation-to-rent story works here. STR has limited HOA constraints (most homes are HOA-free), but city registration is required. Rental vacancy is among the lowest in the metro.

Lenexa

Character: Lenexa has transformed from a sleepy suburb into one of the metro's most deliberately planned growth communities. The Lenexa City Center project — a mixed-use, walkable town center development along Renner Boulevard — represents the most ambitious attempt at urban-style placemaking in the JoCo suburbs. Corporate growth here has been significant: Garmin's campus is a major employer, and the I-435 corridor through Lenexa has attracted distribution, healthcare, and tech tenants.

Housing Stock: Mixed — older ranch neighborhoods in the eastern and central areas, newer planned subdivisions in the west and southwest, and new townhomes and condos near City Center. Construction eras range from 1970s to present.

Price Range: Entry: $260K–$360K. Mid: $360K–$550K. New construction: $450K–$700K+.

Days on Market: Moderate — 18–28 days on average.

Schools: Primarily Shawnee Mission USD 512. De Soto USD 232 serves some western Lenexa parcels — verify at the address level.

Lifestyle: The City Center corridor is where Lenexa is most active — Meadowbrook Park, the Lenexa Rec Center, and a growing restaurant scene make this area increasingly livable without a car. The broader community remains suburban. Commute to downtown KC: 25–35 minutes.

✓ Pros

- Garmin, Cerner/Oracle and corporate employers nearby

- City Center provides urban amenity in suburban setting

- Broad price range — something for most budgets

- Good trail and park infrastructure

- Lower property taxes than some JoCo cities

✗ Cons

- City Center still maturing — some areas feel incomplete

- Western Lenexa can feel remote from KC amenities

- I-435 traffic through the corporate corridor

- School district boundary complexity in west Lenexa

💼 Investor Data — Lenexa

Corporate employment base drives consistent rental demand. City Center condos/townhomes have emerging STR potential — verify with Lenexa city regulations before purchasing. Good cash flow fundamentals in older east Lenexa neighborhoods. BRRRR potential exists on older ranch neighborhoods.

Olathe

Character: Olathe is the county seat of Johnson County and the largest city in JoCo by land area. It's the family-values, middle-market backbone of the Kansas side — well-run municipal government, the Olathe USD 233 school district with consistent academic ratings, and a genuine sense of community identity. Olathe is where you find the best combination of Johnson County quality and accessible pricing.

Housing Stock: Enormous variety. Mid-1980s through 2010s planned subdivisions dominate, with new construction continuing in the southwest. Lot sizes are generally more generous than Overland Park at the same price point.

Price Range: Entry: $240K–$325K. Mid: $325K–$480K. Move-up: $480K–$700K. New construction: $400K–$800K+.

Days on Market: Fast — Olathe competes with OP for quick sales in the under-$400K tier.

Schools: Olathe USD 233 operates Olathe North, Olathe East, Olathe Northwest, Olathe South, and Olathe West high schools. The district is large and academically solid — strong athletics, good STEM programs. Not Blue Valley, but a strong district by any statewide measure. Saint Thomas Aquinas Catholic High School in Olathe is among the most academically regarded private schools in the metro.

Lifestyle: AdventHealth Olathe (hospital) is a major employer. Sar-Ko-Par Meadows Park, Lake Olathe, and Mahaffie Farmstead provide recreation. Old Town Olathe is a small but growing restaurant and entertainment district. Commute to downtown KC: 30–40 minutes.

✓ Pros

- Best price-per-square-foot value in JoCo

- Olathe USD 233 — solid district, multiple high school options

- Saint Thomas Aquinas private school option

- Large lot sizes relative to price

- Lake Olathe and trail access for outdoor recreation

- Strong municipal services and city governance

✗ Cons

- Longer commute to downtown KC vs. north JoCo

- Not Blue Valley — buyers who specifically want BV schools will look further south

- Some older neighborhoods showing deferred maintenance

- Less destination dining/retail than Overland Park or Leawood

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Strong | Best first-time inventory in JoCo; entry points accessible; lower taxes than MO side for comparable quality |

| Upsizer | Strong | Excellent move-up inventory and lot sizes; growing family sweet spot |

| Downsizer | Moderate | Some patio home communities; fewer amenity-rich 55+ options |

| Investor | Strong | Best GRM math in JoCo; strong rental demand from employees priced out of OP |

| Luxury | Moderate | New construction luxury exists but Leawood/south OP are the prestige addresses |

| Relocator | Strong | JoCo quality without JoCo premium — excellent value proposition for out-of-state buyers |

💼 Investor Data — Olathe

Among the best cap rate opportunities in Johnson County. Rental demand is driven by Olathe's employment base and its position as the most affordable major JoCo city. Strong BRRRR candidates in older east Olathe neighborhoods. Olathe requires rental property registration. STR limited by HOA covenants in most planned subdivisions.

Shawnee

Character: Shawnee is the underappreciated workhorse of northern Johnson County. It borders Lenexa to the south and Kansas City, KS to the north, making it a crossroads community with a blue-collar heart that has been steadily gentrifying. The community is more down-to-earth than Overland Park or Leawood, and that's precisely its draw — character, value, and access without the pretense.

Housing Stock: Ranch homes, bi-levels, and split-entries from the 1950s–1980s in the eastern neighborhoods, transitioning to newer planned developments in the west near K-7. Some townhome and condo development along major corridors.

Price Range: Entry: $210K–$300K. Mid: $300K–$450K. Premium: $450K–$600K.

Schools: Shawnee Mission USD 512 across most of the city; small portions in De Soto USD 232 in the far west.

Lifestyle: Mill Creek in Shawnee (now Shawnee Mission Park area) provides the largest single park in JoCo. Shawnee Town 1929 is a local attraction. The 75th Street corridor has a growing restaurant scene. Commute to downtown KC: 20–30 minutes.

✓ Pros

- Most affordable JoCo entry points on the north end

- SMSD schools at competitive price points

- Shawnee Mission Park — largest park in JoCo

- Shorter commute to downtown KC than south JoCo

- Genuine community character — not cookie-cutter

✗ Cons

- Aging housing stock requires maintenance budget

- Some eastern Shawnee neighborhoods border lower-value KCK areas

- Limited high-end retail and dining within city

- Some flood risk near Mill Creek drainage areas

💼 Investor Data — Shawnee

Excellent investor market. Lower purchase prices relative to rents produce some of the best cap rates in Johnson County. BRRRR works well on 1960s–1980s ranches. Watch flood zone maps carefully in low-lying areas near Mill Creek tributaries.

Merriam, Mission & Roeland Park

Character: These three small, densely developed JoCo cities along the state line and Johnson Drive corridor are KC's version of inner-ring suburbs — compact, walkable by JoCo standards, with older housing stock and a demographic tilt toward young professionals, renters, and creatives who want Johnson County without Overland Park prices or aesthetics. Mission and Roeland Park in particular have become local favorites for buyers who want character and community over newness.

Housing Stock: Predominantly 800–1,600 sq ft ranches, bungalows, and Cape Cods from the 1940s–1970s. Some infill townhome development in Mission and Roeland Park. Lot sizes are small.

Price Range: Entry: $175K–$260K. Mid: $260K–$380K. Renovated premium: $380K–$500K.

Schools: Shawnee Mission USD 512 — including Shawnee Mission West High School feeder. Mission Catholic (private, K-8) in Mission.

Lifestyle: The Johnson Drive corridor has excellent independent dining and retail. Farmers markets, walkable parks, strong neighborhood associations. These cities feel like neighborhoods more than suburbs. Commute to downtown KC: 15–22 minutes — the shortest in JoCo.

✓ Pros

- Lowest price points in JoCo — accessible entry for first-timers

- Best walkability in northern JoCo

- Short commute to downtown KC

- Strong community identity; active neighborhood associations

- SMSD access at lowest JoCo price points

✗ Cons

- Small homes — limited square footage for growing families

- Aging infrastructure; older sewer systems

- Some commercial noise/light on major corridors

- Limited parking in some areas

💼 Investor Data — Merriam / Mission / Roeland Park

Among the best cash flow opportunities in JoCo. Low purchase prices, high occupancy, and young professional/renter demographic. STR has growing viability in Roeland Park (verify city regulations). BRRRR on original ranches — some of the best renovation margins in the Kansas metro. Watch for foundation issues in older stock.

Gardner & Spring Hill

Character: Gardner and Spring Hill represent the affordability frontier of Johnson County — still technically within JoCo, still served by respected school districts, but priced like Cass County. If you need JoCo schools at Missouri-side prices, this is where to look. Growth here has been explosive — both cities have seen significant new-construction investment as buyers get priced out of Olathe and central OP.

Housing Stock: New construction dominates, with older downtown Gardner stock offering renovation opportunities. Most product is 1,400–2,600 sq ft two-stories on planned subdivision lots.

Price Range: Entry: $220K–$300K. Mid: $300K–$430K. New construction: $380K–$550K.

Schools: Gardner USD 231 — not Blue Valley or Shawnee Mission, but a competitive mid-tier Kansas district with improving scores. Spring Hill USD 230 serves Spring Hill.

Lifestyle: Car-dependent. Still developing retail and restaurant infrastructure. Access to I-35 makes the commute to central JoCo or downtown KC (40–50 minutes) manageable. The Moonrise Beer Garden and local businesses in downtown Gardner give it some identity.

✓ Pros

- Johnson County address at entry-level prices

- New construction quality without new-construction premium of north OP

- Fast-growing equity market as growth continues south

- Lower density — larger lots at price point

✗ Cons

- Long commute to KC employment centers (40–55 minutes to downtown)

- School districts don't match Blue Valley or SM caliber

- Infrastructure can lag population growth in boom periods

- Minimal walkability or urban amenity

💼 Investor Data — Gardner / Spring Hill

Good long-term appreciation play as the JoCo growth corridor continues south. Rental demand growing with population but tenant pool is thinner than north JoCo. New construction makes BRRRR less relevant. Better for buy-and-hold appreciation than immediate cash flow.

Jackson County, Missouri

The heart of the Missouri side — home to downtown KC, the historic neighborhoods that give the metro its character, and the sprawling suburb of Lee's Summit. The most diverse market in terms of buyer types, price points, and neighborhood character.

Jackson County is the beating heart of KC proper. It contains the downtown skyline, the historic neighborhoods that give KC its cultural identity, and one of the metro's fastest-growing suburbs in Lee's Summit. The county's breadth — from East KC's distressed but improving core to Brookside's polished bungalows to Lee's Summit's master-planned communities — means it serves almost every buyer type simultaneously. Understanding which Jackson County you're buying into is the key to this market.

Waldo & Brookside

Character: These two adjacent neighborhoods south of the Plaza are the most beloved addresses in all of Kansas City, Missouri. Brookside — centered on Brookside Boulevard and its cluster of independent shops and restaurants — has the feel of a small urban village embedded in a city. Waldo, its slightly more affordable neighbor, shares the same building stock and general vibe but with a slightly younger, more renter-mixed demographic. These neighborhoods attract people who could afford Johnson County but specifically don't want it.

Housing Stock: Primarily Tudor, Colonial, and craftsman bungalows from the 1920s–1950s. Two-story homes on tree-lined streets with detached garages and front porches. Lot sizes are modest. Renovated homes are common; unrenovated homes represent the opportunity.

Price Range: Waldo entry: $225K–$320K. Brookside entry: $310K–$420K. Mid: $420K–$600K. Premium renovated: $600K–$900K+.

Days on Market: Very fast — 7–18 days for priced-right homes. Brookside routinely sees multiple offers.

Appreciation: Strong and consistent — among the best in KCMO over the past decade.

School Information

Kansas City, Missouri School District (KCMSD) serves these neighborhoods. The district has faced significant challenges historically, losing accreditation in the 2010s (now provisionally accredited). Most private-school-minded families here send their children to private options: Notre Dame de Sion (close proximity), Pembroke Hill (Wornall Road), Barstow School, and St. Elizabeth Catholic School. The private school culture in Brookside is robust — budget for tuition if schools are a priority.

Lifestyle & Amenities

The Brookside retail district — Crabby's, the Novel bookshop, Room 39, Epicerie — is one of KC's best walkable retail nodes. Waldo's 75th Street corridor has excellent restaurants and bars. Loose Park (adjacent to Brookside) is a beloved 75-acre park with tennis courts, a rose garden, and a pond. Ward Parkway Boulevard provides a green spine south to the plaza. Commute to downtown KC: 12–20 minutes. KU Health System: 8–15 minutes.

✓ Pros

- Best walkability and neighborhood character in KCMO

- Proximity to Plaza, KU Med, and downtown

- Genuine architectural character — no two homes look the same

- Strong community identity and neighborhood associations

- Excellent renovation upside on unrenovated stock

- Strong appreciation trajectory — proximity to quality anchors value

✗ Cons

- KCMSD public schools — most families will need private school budget

- Older homes require ongoing maintenance commitment

- Sewer scope essential — lateral failures common in this era of construction

- Radon testing critical — older basements in geological hotspot area

- Competition is fierce; less inventory than suburban markets

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Moderate | Waldo has accessible entry points; Brookside is harder for first-timers to compete |

| Upsizer | Strong | Move-up to renovated Brookside — a prestige KCMO address |

| Downsizer | Moderate | Good walkability appeal; stairs in most homes; limited maintenance-free options |

| Investor | Strong | Excellent BRRRR plays; rental demand from hospital corridor; strong appreciation |

| Luxury | Moderate | Upper-end Brookside competes with Plaza — legitimate luxury at the top |

| Relocator | Strong | KC's most "wow" neighborhoods — relocators love the character |

💼 Investor Data — Waldo / Brookside

BRRRR is alive here. Unrenovated Waldo bungalows can be acquired in the $200K–$270K range and renovated for $60K–$100K to achieve post-renovation values of $360K–$450K. Hospital corridor proximity keeps rental vacancy extremely low. STR viability is strong for Brookside — KC has a growing STR tourism market and proximity to the Plaza is a selling point. Sewer laterals are your #1 hidden cost item — budget $8K–$15K per unit.

Midtown & Westport

Character: Midtown is the urban core south of downtown — a mixed-use tapestry of apartment buildings, single-family streets, medical institutions, and the Crown Center / Hallmark campus. Westport is KC's original entertainment district, with a dense concentration of bars, restaurants, and nightlife that draws the young professional crowd. The neighborhoods immediately surrounding Westport — Roanoke, Valentine, Hyde Park — are some of KCMO's most interesting residential streets.

Housing Stock: Heavy mix of apartment stock and single-family. Single-family homes in surrounding streets (Roanoke, Hyde Park) are craftsman bungalows and Victorians from the early 1900s. Significant renovation upside exists on underutilized stock.

Price Range: Entry SFR: $175K–$280K. Mid: $280K–$430K. Premium: $430K–$650K. Condos: $150K–$400K.

Schools: KCMSD — same school district considerations as Brookside. Private options are the go-to for families: Barstow, Pembroke Hill, Saint Paul's Episcopal Day School.

Lifestyle: KC's most urban living environment. Westport bars and restaurants are within walking distance. Crown Center, Power & Light, and the Sprint Center are close. KU Medical Center is accessible. Commute to downtown: 8–15 minutes.

✓ Pros

- Most urban, walkable KC living environment

- Best access to KC entertainment, arts, and dining

- Short commute to downtown and hospital corridor

- Strong investor returns on multi-family and SFR

- Victorian and craftsman architectural stock

✗ Cons

- KCMSD schools — private school essential for families

- Urban crime risk — research specific blocks carefully

- Noise from Westport entertainment district

- Parking constraints in some areas

💼 Investor Data — Midtown / Westport

Among the highest cap rates in the metro on a risk-adjusted basis for investors comfortable with urban markets. STR/Airbnb has real viability near Westport and Crown Center — KC does have a meaningful convention and tourism market. Multi-family investors should note KCMO rental property registration and inspection requirements. Crime risk varies significantly block-by-block — drive the specific streets before committing.

Plaza / Country Club District

Character: The Country Club District — developed by J.C. Nichols beginning in the 1910s — is one of America's first planned residential communities and remains Kansas City's most architecturally significant address. The streets surrounding the Country Club Plaza shopping district are lined with Spanish Colonial, Tudor, and Georgian revival homes of extraordinary craftsmanship. This is KCMO's answer to JoCo's Leawood — prestige, history, and proximity to everything.

Housing Stock: 1910s–1940s period architecture — Tudor revivals, Georgian colonials, and Spanish tiles. Homes range from 1,800 to 8,000+ sq ft. Many have been meticulously maintained; others offer significant renovation upside at high price points.

Price Range: Entry: $450K–$650K. Mid luxury: $700K–$1.2M. Upper: $1.2M–$4M+.

Days on Market: Moderate — 25–45 days. The buyer pool at this price is deep but not infinite.

Schools: KCMSD — private school is essentially universal at this income level. Pembroke Hill (on Ward Parkway), Barstow, and Notre Dame de Sion are the primary feeders for this community.

Lifestyle: The Country Club Plaza itself — 15 blocks of Spanish-themed retail, dining, and entertainment — is literally in the backyard of these neighborhoods. The Nelson-Atkins Museum of Art is adjacent. Ward Parkway's park medians provide a linear green corridor. Commute to downtown: 12–18 minutes.

✓ Pros

- Kansas City's most architecturally significant residential neighborhoods

- Walking distance to the Plaza, Nelson-Atkins, and Loose Park

- Period architecture that can't be replicated

- High-quality buyer pool = strong resale market

- Proximity to KU Health System and Children's Mercy

✗ Cons

- KCMSD public schools — private school is effectively mandatory

- High maintenance costs on period homes — HVAC, roofing, masonry

- Flood risk in low-lying areas near Brush Creek — check FEMA maps

- KCMO property taxes higher than JoCo

- Parking challenges near the Plaza corridor

💼 Investor Data — Plaza / Country Club District

Corporate executive relocation rental demand is strong here. STR/Airbnb has legitimate upside near the Plaza — KC is a growing tourism and convention market. Cap rates are compressed by high purchase prices, but appreciation is a strong supporting thesis. Flood zone status must be verified for each property — Brush Creek has a history of flooding. Insurance costs can be significant in flood-zone-adjacent properties.

Northland / North Kansas City

Character: "The Northland" is what KC locals call the area north of the Missouri River — primarily Clay and Platte counties geographically, though the concept extends into the northernmost reaches of KC proper. North Kansas City (NKC) proper is a separate municipality known for its renovated industrial-district aesthetic: brick warehouses converted to restaurants, breweries, and offices have made it a destination. The Northland's residential markets are predominantly suburban, family-oriented, and notably more affordable than south KC equivalents.

Housing Stock: Ranch homes and two-stories from the 1970s–1990s in most established Northland neighborhoods. New construction in outer Clay and Platte County. NKC proper has some loft-style residential conversion.

Price Range: Entry: $185K–$280K. Mid: $280K–$420K. Move-up: $420K–$600K.

Schools: North Kansas City USD 74 (covering NKC and surrounding areas) — a solid Missouri district with strong vocational and arts programs. Liberty USD 53 serves Liberty proper (reviewed under Clay County).

Lifestyle: NKC's restaurant and brewery scene along Armour Road has become a legitimate destination. The Missouri River provides boating access. Commute to downtown KC: 15–25 minutes from most Northland locations.

✓ Pros

- Affordable relative to south KC equivalents

- NKC's emerging arts/brewery scene adds character

- Reasonable commute to downtown over the river bridges

- More space per dollar than south KCMO

✗ Cons

- Traffic bottleneck over Missouri River bridges at rush hour

- Perception barrier — "North of the river" has historically carried stigma

- Less developed retail/dining in outer Northland suburbs

- Some flood risk near river bottom land

💼 Investor Data — Northland / NKC

Strong investor market. NKC has emerging STR viability driven by the brewery/arts district. Older Northland ranches provide BRRRR opportunities. Missouri's landlord-friendly laws make this an easier operating environment than the Kansas side for some investors. Check FEMA flood maps for river-adjacent properties.

Lee's Summit

Character: Lee's Summit is the Kansas City metro's most complete suburban community — a city of roughly 100,000 with a charming historic downtown, one of Missouri's top school districts, and a housing market that delivers exceptional quality-of-life value. It's where young families who want the full suburban package — schools, space, safety, community — but can't (or don't want to) pay JoCo prices end up. Lakewood is its luxury gem: a master-planned lakefront community that rivals anything in Johnson County at a slightly lower price point.

Housing Stock: Enormous range — historic 1920s–1940s homes in downtown LS, 1980s–2000s ranch and two-stories in central LS, and new construction in outer subdivisions. Lakewood is new-to-recent construction with lake access and community amenities.

Price Range: Entry: $220K–$320K. Mid: $320K–$500K. Lakewood/luxury: $500K–$1.2M.

Days on Market: Fast — Lee's Summit consistently has among the lowest days-on-market in the KCMO suburbs.

Appreciation: Strong — LS has been one of KCMO's best appreciation stories over the past decade.

School Information

Lee's Summit R-7 School District is one of Missouri's top-rated districts — consistently ranked #1 or #2 statewide by Niche and US News. Lee's Summit North and Lee's Summit West are both Blue Ribbon schools. The district's graduation rates, college placement, and standardized test scores rival the best in JoCo. This school district is the #1 driver of demand in the market.

Lifestyle & Amenities

Historic downtown Lee's Summit has a genuine walkable main street feel — independently owned restaurants, a farmers market, and community events. Lake Jacomo and Longview Lake provide boating, fishing, and swimming. Cerner/Oracle Health's campus in south Lee's Summit is a major employer. Commute to downtown KC: 30–40 minutes via I-470. The new streetcar extension discussions may eventually reach this direction.

✓ Pros

- One of Missouri's best school districts (LS R-7)

- Charming historic downtown — rare in suburban KC

- Lakewood luxury community at JoCo prices

- Multiple lakes and outdoor recreation

- Strong appreciation in every price tier

- More affordable than comparable JoCo addresses

✗ Cons

- Commute to downtown KC (30–40 min) longer than north JoCo

- Traffic on I-470 during peak hours

- Less luxury retail than Leawood/OP

- Some outer suburbs feel generic without LS character

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Strong | Best school district access at accessible prices in KCMO |

| Upsizer | Strong | The primary move-up destination on the Missouri side for families |

| Downsizer | Moderate | Lakewood patio homes are a strong option; limited broader 55+ inventory |

| Investor | Strong | Top school district drives exceptionally low rental vacancy; strong appreciation |

| Luxury | Strong | Lakewood competes with south Overland Park luxury at a price advantage |

| Relocator | Strong | Highest-quality schools + affordable price = top relocation recommendation on MO side |

💼 Investor Data — Lee's Summit

LS R-7 school district drives rental demand from families who aren't yet buying. Rental vacancy is among the lowest in KCMO. STR has growing viability near the downtown and lake corridors. Cerner/Oracle campus drives corporate housing demand. Strong long-term appreciation thesis. Missouri landlord-tenant laws are investor-friendly compared to some states.

Independence, Blue Springs, Raytown & Grandview

Independence is one of the KC metro's most complex markets — it's the hometown of Harry Truman, with a historic square that has genuine charm, but it's also a large city with wide variation in neighborhood quality. The Englewood neighborhood near the historic square is gentrifying; outer Independence near the I-70 corridor is more working-class suburban. Price points are among the metro's most accessible ($130K–$280K range for entry), making it a first-time buyer and investor market primarily.

Blue Springs is Independence's more polished neighbor to the east — a well-regarded suburb with Blue Springs R-IV School District (solid, not elite) and a strong family demographic. Price points: $220K–$400K for most of the market.

Raytown is one of KC's classic inner-ring suburb stories — once solidly middle-class, now attracting renovation buyers and investors drawn by extremely affordable pricing and proximity to south KC. Entry: $100K–$200K. Renovation potential is significant.

Grandview in the south is similarly positioned — workforce housing at the metro's lowest price points ($120K–$220K), with Grandview C-4 School District serving the area.

Schools

School quality varies significantly across these communities. Blue Springs R-IV is the strongest of the group. Independence R-VII has been improving but remains a work in progress. Raytown C-2 has faced challenges. Always verify the specific school and district rating for any address you're considering.

✓ Pros

- Metro's most affordable price points — entry access for all buyers

- Independence historic square has genuine charm

- Blue Springs R-IV: solid school district at low price point

- High investor upside in Raytown and Independence

✗ Cons

- School district quality varies widely — research each address

- Some neighborhoods have high crime and code enforcement issues

- Deferred maintenance common in older Independence and Raytown stock

- Limited upscale retail and dining in some areas

💼 Investor Data — East/South Jackson County

Highest cap rates in the metro — but with commensurate management risk. Workforce housing demand is robust. Tenant screening and professional management are more important here than in premium submarkets. BRRRR is very active in Raytown and Independence. Know your exit — appreciation thesis is less certain than in growth corridors.

Wyandotte County, Kansas

The most underrated story in the KC metro — a county undergoing one of the most significant economic transformations in the region's history, driven by billion-dollar investments and strategic development.

Wyandotte County — home to Kansas City, Kansas (KCK) — has long been the most economically challenged county in the metro. But that narrative is changing rapidly. The Village West / Kansas Speedway entertainment and retail corridor has already transformed the western edge of the county. And the Panasonic EV battery manufacturing plant — a $4 billion investment announced in 2022 and now under construction — represents the largest economic development project in Kansas history. This plant, financed in part through the state's STAR bond mechanism, will bring thousands of jobs and a historic wave of workforce housing demand to a county that has never experienced anything like it.

Kansas City, Kansas (KCK)

Character: KCK is a working-class city with a complex history — once a thriving meatpacking and rail center, it experienced significant economic decline in the second half of the 20th century. Today it's a city of neighborhoods that vary enormously in quality and trajectory. Some areas near the Village West corridor and Argentine neighborhood are showing genuine revitalization; other areas in east KCK remain distressed.

Housing Stock: Predominantly bungalows, craftsman-style homes, and modest ranch homes from the 1920s–1960s. Very affordable acquisition prices. Many homes require significant rehabilitation.

Price Range: Entry: $80K–$150K. Renovated: $160K–$280K. Village West adjacent: $200K–$350K.

Schools: Kansas City, Kansas Public Schools (USD 500) — the district faces significant challenges. Families with school-age children who are buying in KCK for investment purposes typically expect to supplement with private schooling or wait for the school district to improve as the tax base grows.

Village West / Kansas Speedway: The Western Wyandotte Speedway area includes Kansas Speedway, Sporting KC's Children's Mercy Park, a Bass Pro Shop, T-Mobile Center, and extensive retail/entertainment. This corridor drives significant hospitality and retail employment and has stabilized the western county's economic base.

✓ Pros

- Metro's lowest acquisition prices — entry is highly accessible

- Panasonic plant proximity — potentially transformational

- Village West employment base

- High cash flow potential for investors who manage risk

- Speculation/appreciation upside if transformation continues

✗ Cons

- High property tax rate relative to home values

- School district significant challenge

- Crime risk varies widely by neighborhood

- Infrastructure needs in older areas

- Transformation timeline is uncertain — speculative play

💼 Investor Data — KCK

Highest cap rates in the metro. Workforce housing demand is structural and growing with Panasonic-related job growth. Kansas has different landlord-tenant laws than Missouri — eviction process is relatively efficient. STR viability near Village West is real — Kansas Speedway races and Sporting KC games drive weekend demand. Significant due diligence on individual properties is critical — deferred maintenance risk is high. Consider professional management essential in this market.

Bonner Springs & Edwardsville

Character: Bonner Springs is Wyandotte County's most livable small community — a river town on the Kansas River with a historic downtown, relatively stable neighborhoods, and Basehor-Linwood USD 204 school district options in adjacent areas that dramatically outperform USD 500. Edwardsville, adjacent to Bonner Springs, is a tiny residential community with affordable homes and quiet streets.

Housing Stock: Modest ranches and two-stories. Some newer construction on the western edges. River proximity creates both character and flood risk.

Price Range: Entry: $140K–$220K. Mid: $220K–$330K.

Schools: Bonner Springs USD 204 — a significantly better performing district than KCK's USD 500. This alone makes Bonner Springs more attractive for families in Wyandotte County.

💼 Investor Data — Bonner Springs / Edwardsville

Good cash flow fundamentals with lower management risk than inner KCK. Better school district makes it easier to attract stable family tenants. Watch FEMA flood maps carefully — Kansas River flooding is a real risk for low-lying properties. Verify flood insurance requirements before closing.

Cass County, Missouri

The I-49 corridor growth story — the metro's most affordable new-construction frontier, attracting first-time buyers and growing families willing to trade commute time for space and price.

Cass County is the I-49 corridor story. The highway that runs south from KC through Belton, Raymore, Peculiar, and eventually Harrisonville has become the spine of the metro's most affordable growth market. Families who need more house than they can afford in Jackson or Johnson counties come here — and they've been coming in volume, driving significant new construction activity south of Belton. The county's Missouri property tax rates are manageable, schools are respectable (particularly Raymore-Peculiar R-II), and the quality of new construction is solid.

Belton & Raymore

Character: Belton and Raymore are suburban communities on the I-49 corridor that offer families solid infrastructure, reasonable schools, and significantly more house per dollar than north Jackson County. Raymore in particular has become a strong growth market with new subdivision development and a reputation for being clean, well-maintained, and family-oriented.

Housing Stock: Mix of 1980s–2000s established subdivisions and new construction on the periphery. Homes are typically 1,400–2,600 sq ft, two-story or ranch, on 1/4 to 1/2 acre lots.

Price Range: Entry: $185K–$260K. Mid: $260K–$380K. New construction: $340K–$480K.

Schools: Raymore-Peculiar R-II (Ray-Pec) — one of Missouri's fastest-growing and improving suburban districts. Belton R-V serves Belton. Both are solid mid-tier Missouri districts.

Commute Context: I-49 to downtown KC is 30–45 minutes on a good day; 45–60 minutes in peak traffic. This is the #1 tradeoff buyers must honestly evaluate.

✓ Pros

- Most affordable new construction in the metro

- Ray-Pec schools — growing and improving

- More space per dollar than any comparable north option

- Low crime; family-centric community culture

- MO property tax rates lower than JoCo Kansas

✗ Cons

- Long commute — I-49 traffic south of Grandview is real

- Car-dependent; extremely limited walkability

- Retail and dining options limited vs. north metro

- Slower appreciation trajectory than north/east JoCo

💼 Investor Data — Belton / Raymore

Good cash flow fundamentals on new construction at accessible price points. Tenant quality in family-centric Raymore is strong. Appreciation story is improving as growth continues. Missouri's landlord-friendly eviction process is an investor advantage. Limited STR demand in this market — long-term rental is the play.

Peculiar & Harrisonville

Peculiar (served by Ray-Pec R-II) and Harrisonville (served by Harrisonville R-IX) represent the outer affordability frontier — rural-adjacent communities where buyers get significant land and space at prices that feel like a different market entirely. Entry-level homes in Peculiar start in the $160Ks. Harrisonville is the Cass County seat with its own community identity, courthouse square, and services.

These markets appeal to buyers who work remotely, value land, or have family ties to the area. The commute to metro employment centers (50–75 minutes) limits the buyer pool significantly.

💼 Investor Data — Peculiar / Harrisonville

Thin rental market — tenant pool is smaller. Works for investors with local connections who can fill vacancies efficiently. USDA loan eligibility in many areas (useful for owner-occupant buyers). Not recommended for out-of-area investors without local property management.

Clay County, Missouri

Liberty's suburban polish, Smithville Lake's lifestyle draw, and accessible pricing make Clay County the Missouri side's family-value answer to Johnson County.

Liberty

Character: Liberty is one of the metro's most complete suburban communities — a historic city with a well-preserved downtown square (William Jewell College sits at its heart), one of Missouri's top-rated school districts in Liberty Public Schools USD 53, and a housing market that delivers exceptional quality-of-life per dollar. It's the "Lee's Summit of the Northland" — a well-run, family-focused city with genuine charm.

Housing Stock: Historic homes near downtown and the college, 1980s–2000s planned subdivisions in the broader city, and newer construction in outer Liberty. Wide price range within the city.

Price Range: Entry: $200K–$295K. Mid: $295K–$440K. Move-up: $440K–$650K.

Schools: Liberty Public Schools USD 53 — consistently ranked among Missouri's top 10 districts statewide by Niche. Liberty North and Liberty High School are both well-regarded. The district's academic rigor is a primary driver of Liberty's real estate demand.

Lifestyle: William Jewell College provides a collegiate atmosphere and cultural events. Historic downtown square with dining and retail. Liberty Hospital. Commute to downtown KC: 20–30 minutes via I-35 or I-69.

✓ Pros

- Top-10 Missouri school district — strong academic reputation

- Historic downtown with genuine character

- William Jewell College adds cultural depth

- Shorter commute than south Clay County options

- Broad price range accommodating most buyer types

✗ Cons

- Bridge/river traffic can affect rush-hour commutes south

- Less retail sophistication than JoCo equivalent

- Outer Liberty growth can feel disconnected from city core

💼 Investor Data — Liberty

Liberty school district drives consistent rental demand from families. Very low vacancy rates in the district attendance zones. Student rental demand from William Jewell adds an additional tenant pool. BRRRR opportunities exist in older downtown-adjacent neighborhoods. STR has some viability near downtown Liberty.

Smithville & Smithville Lake

Character: Smithville is the lake lifestyle community of the KC metro. Smithville Lake — a 7,000-acre Corps of Engineers reservoir — is surrounded by communities that attract buyers who want recreation, space, and a slower pace within commuting distance of KC. The lake draws boaters, anglers, and families who want a vacation-home feel as their permanent residence.

Housing Stock: A mix of older lake-adjacent homes, newer custom and semi-custom construction in surrounding subdivisions, and traditional suburban stock in Smithville proper.

Price Range: Entry: $195K–$280K. Mid: $280K–$425K. Lakefront/premium: $425K–$750K+.

Schools: Smithville R-II School District — a smaller district with good performance metrics. Solid, community-oriented schools.

Lifestyle: Smithville Lake State Park, marina access, fishing, sailing, and camping. The Smithville community itself has local dining and events. Commute to downtown KC: 35–45 minutes via I-35.

💼 Investor Data — Smithville Lake

Smithville Lake has legitimate STR viability — weekend lake rental demand from KC residents is real. Lakefront properties can command premium STR rates ($200–$400/night in season). Long-term rental market is thinner. Verify Smithville STR registration requirements. Lakefront property insurance can be elevated.

Kearney & Excelsior Springs

Kearney is a small Clay County community with Kearney R-I schools (solid, community-focused) and affordable pricing in the $175K–$320K range. It serves buyers who want more land and a slower pace while staying connected to the metro via I-35.

Excelsior Springs is a historic spa town east of the metro — known for the Hall of Waters and its mineral springs history. It's an outer-market community with very affordable pricing ($100K–$225K) and a strong sense of historic identity. The commute to KC (40–55 minutes) limits its metro integration, but its price points and character attract buyers who value both.

💼 Investor Data — Kearney / Excelsior Springs

Excelsior Springs has emerging STR potential tied to its historic hotel and spa tourism (The Elms Hotel). Tenant pool is thin — not recommended without local management. Kearney offers better fundamentals with school district draw. Both markets reward locally-connected investors over remote operators.

Platte County, Missouri

KCI airport proximity, Parkville's small-town charm, and Weatherby Lake's lifestyle appeal make Platte County the Northland's most distinctive residential market.

Parkville

Character: Parkville is the KC metro's best-kept secret — a small Missouri River town with a genuine historic main street (Main Street Parkville), Park University, English Landing Park along the river, and a residential market that delivers character, school quality, and relative affordability in one package. It feels like a small town that happens to be 20 minutes from downtown KC. Residents are fiercely loyal — turnover is low because people don't want to leave.

Housing Stock: Eclectic mix of historic homes near downtown Parkville, New Mark master-planned community (mid-2000s construction), English Landing estates, and rural residential on larger parcels.

Price Range: Entry: $230K–$320K. Mid: $320K–$475K. New Mark / English Landing: $500K–$1M+.

Schools: Park Hill School District — consistently one of Missouri's top 5 school districts statewide. Park Hill High School and Park Hill South High School are both excellent. The district is a major driver of Parkville's real estate demand.

KCI Airport Proximity: A 10–15 minute drive to KCI Airport from most Parkville addresses. For frequent travelers, this is a genuine lifestyle advantage that buyers from other cities immediately recognize.

Lifestyle: English Landing Park along the Missouri River is a premier green space. Main Street Parkville has excellent independent dining, a brewery, and community events. Park University adds cultural programming. Commute to downtown KC: 20–28 minutes via I-435 or Highway 9.

✓ Pros

- Park Hill School District — top 5 in Missouri consistently

- Genuine small-town charm — authentic main street

- KCI proximity — 10 minutes to the airport

- Missouri River park and trail access

- Relatively affordable compared to JoCo equivalents

- Very low turnover — residents stay long-term

✗ Cons

- Limited high-end retail (must go to JoCo or downtown for luxury shopping)

- Some flood risk in river-adjacent areas

- Traffic on Highway 9 / I-435 interchange can be congested

- Less new-construction selection than JoCo equivalents

| Buyer Type | Fit | Notes |

|---|---|---|

| First-Timer | Moderate | Entry price points accessible; Park Hill schools worth the effort |

| Upsizer | Strong | New Mark community is a top Northland move-up destination |

| Downsizer | Strong | Walkable main street is a genuine draw; low-maintenance options near town center |

| Investor | Moderate | Low turnover makes it harder to acquire rental properties but strong fundamentals once owned |

| Luxury | Strong | English Landing and New Mark estates compete with JoCo at better prices |

| Relocator | Strong | Airport proximity is a unique advantage; frequently surprises relocators with quality |

💼 Investor Data — Parkville

Park Hill school district drives strong rental demand from families — lowest vacancy rates in Platte County. STR has emerging viability near main street — Park University and river tourism generate demand. Properties are rarely distressed enough for BRRRR — this is a buy-and-hold appreciation market. Airport proximity appeals to corporate relocation renters.

Platte City, Riverside & Weatherby Lake

Platte City is the county seat — a small, modest community with affordable housing ($150K–$280K) and Platte County R-III schools (solid but smaller district). Its appeal is affordability and KCI proximity.

Riverside is a small municipality along the Missouri River with mixed residential stock and proximity to the river. It's seen some revitalization investment and benefits from KCI access.

Weatherby Lake is a private lake community — a gated, homeowner-association-governed neighborhood surrounding a 300-acre private lake. It's an enclave of mid-to-upper-range homes ($350K–$750K) with lake access, a community beach, and club amenities. Private lake access is Weatherby Lake's unique selling proposition in a market where lake lifestyle usually requires driving to Smithville or Lake of the Ozarks.

💼 Investor Data — Platte City / Weatherby Lake

Weatherby Lake HOA restricts rentals significantly — verify before purchasing as investment. Platte City is a better cash flow market. KCI airport employees represent a consistent rental tenant base for both markets. STR is limited by HOA in Weatherby Lake.

Miami County, Kansas

The affordability corridor — buyers priced out of Johnson County find their entry to the Kansas side here, with room to grow as the I-35 growth corridor extends south.

Miami County lies directly south of Johnson County on I-35 — which means it sits in the direct path of KC's southward growth corridor. Paola (the county seat) and Osawatomie are rural communities by current standards, but their proximity to Gardner and Spring Hill means that as those communities grow south, Miami County becomes increasingly attractive to commuters and remote workers.

Paola & Osawatomie

Paola has a well-preserved historic downtown square, Miamian R-I schools, and entry-level pricing that attracts buyers who've been fully priced out of JoCo. Home prices range from $120K–$280K for most of the market. The commute to JoCo employment (40–55 minutes on I-35) is the primary barrier.

Osawatomie is a smaller community further south with very affordable pricing ($90K–$180K) and Osawatomie USD 367 schools. It's primarily a remote-worker or retiree market given the commute distance.

💼 Investor Data — Miami County

High cap rates but thin rental market. Not recommended without local connections and management in place. USDA loan eligibility in many Miami County areas — a buyer program advantage. Long-term appreciation speculation is the primary thesis; current cash flow requires active management.

The Home Buying Process — Step by Step

Every real estate transaction follows a predictable sequence — but the Kansas City metro has specific nuances in Kansas and Missouri that affect how each stage plays out. Here's exactly what to expect, from the moment you start thinking about buying to the day you get your keys.

Financial Readiness — Before You Look at a Single Home

The biggest mistake KC buyers make is falling in love with a home before knowing with certainty what they can afford and what it will actually cost. Don't browse Zillow until you've done this work.

Credit Score Impact

Your credit score directly determines your mortgage rate tier. In a market where rates have been in the 6–7%+ range, the difference between a 680 and a 760 score can represent $200–$400/month on a $400K loan. Get your credit report (annualcreditreport.com), dispute any errors at least 90 days before you plan to buy, and avoid opening new credit lines or making large purchases before and during your transaction.

Down Payment Options

- Conventional (3–20% down): Standard route for most buyers. At less than 20%, you'll pay Private Mortgage Insurance (PMI) — typically 0.5–1.5% of the loan annually — until you reach 20% equity.

- FHA (3.5% down): Accessible for credit scores as low as 580. Requires mortgage insurance for the life of the loan in most cases. Current FHA loan limit for the KC metro is approximately $498,000 — confirm current limits with your lender.

- VA (0% down): Exceptional program for eligible veterans and active-duty service members. No PMI, competitive rates. Fort Leavenworth proximity makes VA loans particularly relevant in the northern KC market.

- USDA (0% down): Rural development loans with 0% down payment. Certain KC metro areas qualify — particularly outer Cass County, Miami County, and rural Clay/Platte county areas. Income limits apply. Ask your lender specifically about USDA eligibility in your target area.

- KHRC (Kansas Housing Resources Corporation): First-time buyer programs in Kansas offering down payment assistance and below-market interest rates. Income and purchase price limits apply. Visit kshousingcorp.org for current programs.

- MHDC (Missouri Housing Development Commission): Missouri's equivalent program — down payment assistance, below-market rate first mortgages, and tax credit programs for qualifying buyers. Visit mhdc.com for current offerings.

First-Time Buyer Program Quick Reference

| Program | State | Key Benefit |

|---|---|---|

| KHRC First-Time Buyer | Kansas | Up to 20% DPA + below-market rate |

| MHDC First Place Loan | Missouri | Up to $10K forgivable DPA |

| Johnson County HOME Program | Johnson Co. KS | Closing cost assistance |

| City of KCMO DPA | KCMO | Grants in targeted areas |

| FHA 203(b) | Federal | 3.5% down, flexible credit |

| VA Home Loan | Veterans | Zero down, no PMI |

| USDA Rural Loan | Federal | Zero down — outer KC suburbs eligible |

Pre-Approved vs. Pre-Qualified